INFOGRAPH: Iron ore price softening on less demand

Source:Mysteel Sep 09, 2021 14:01

- ABSTRACT

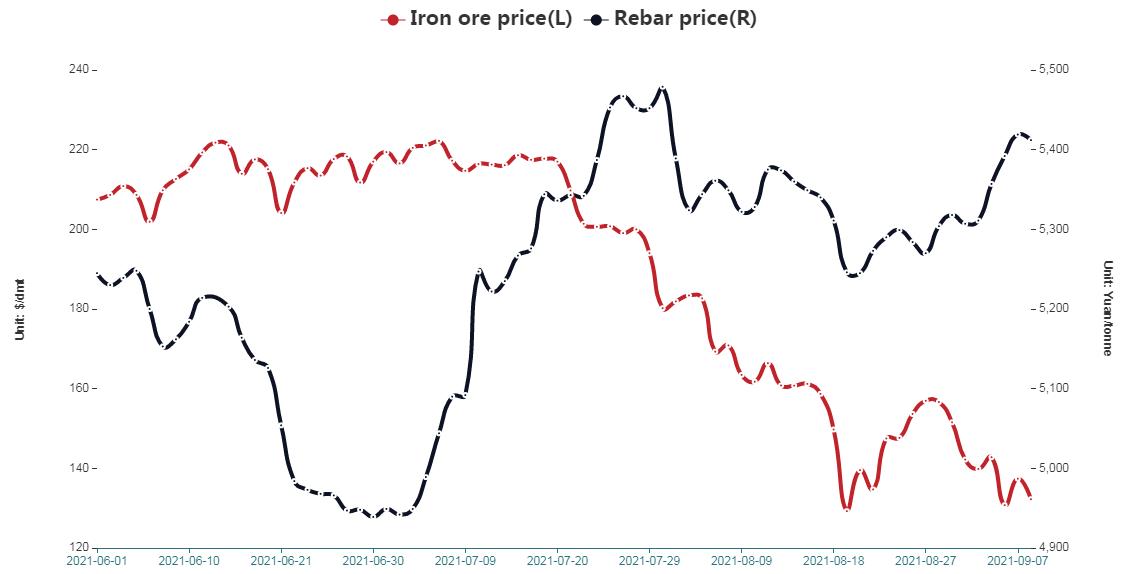

- China’s rebar and imported iron ore prices have diverged more substantially recently, which has not caught the market by surprise, as improvement in spot steel demand in September is expected to lend support to the steel prices but lower steel output on the other hand is dampening raw material prices with iron ore in particular, Mysteel Global noted.

As of September 8, Mysteel SEADEX 62% Australian Fines fluctuated down to $132.25/dmt CFR Qingdao, falling $38.6/dmt on month or $101.5/dmt from its all-time high on May 12, mainly as demand from the Chinese steel mills has shrunk with their cautiousness amid Beijing’s call for lower steel output for 2021 as well as actual crude steel cuts among many producers.

In contrast, China’s national price of HRB400E 20mm dia rebar under Mysteel’s assessment as a representative of the country’s spot steel market, however, strengthened Yuan 63/tonne ($9.7/t) on month to Yuan 5,412/t as of September 8, though it was Yuan 936/t lower than its all-time high on May 12.

- China’s steel output did show declines, as over August 27-September 2, blast furnace capacity utilization among the 247 Chinese steel mills under Mysteel’s survey hovered at 85.45%, much lower than the over 90% for May-June and also 9.07 percentage points lower on year.

- Under the circumstances, and the prevalent pessimism where steel output and iron ore consumption are concerned, Chinese steel mills have been very conscious of their in-house iron ore stocks and rather cautious in iron ore procurement, so as to minimize exposure to pricing risks, to free cash flow and to reduce costs in raw materials. Some mills have also been re-selling any surplus tonnage from their long-term deal supplies.

- As of September 2, inventories of imported iron ore at the 247 mills in all forms including the volumes at steelworks, port stockyards and on the water had declined for the sixth week, down another 1.29 million tonnes to 104.23 million tonnes, or a new low since mid-March 2020.

- For the foreseeable future, iron ore demand from the Chinese steel mills seems hard to rebound for the rest of the year, as the curbing on steel output nationwide may be wider in scope and more stringent in degree, and on top of these, winter restrictive measures may be in place starting October, Mysteel Global understood from the market.

Post time: Sep-09-2021